To understand the prospects for financial markets in 2019, we need to remember the uncertainty and volatility of 2018. The year 2018 will be remembered as one of the difficult years to manage, but even in other difficult periods there have always been some "active refuges" where It has been possible to earn money (or at least not lose it). In 2018, there were drops in the prices of fixed income shares (Global Investment Grade -3.4% in the year), (S&P500 -7.03% in the year, Ibex -15.4% in the year; Stoxx600 -13.7% in the year or MSCI China -21.2% in the year) or even gold (-3.7% in the year).

The key factors that dominated 2018 were diverse: Trump's trade war; the umpteenth crisis in the EU for Italy; Brexit; crisis in emerging markets; rise in interest rates in the United States and fears of a globalised economic slowdown, to name the most significant ones. The sense of panic that happened in many moments is unjustified. To this, we would add the correction in prices in the shares of the technology sector. The sum of factors that we mentioned at the beginning, caused the perfect storm in the fourth quarter of 2018.

OUTLOOK FOR 2019

What is the panorama in 2019? There is evidence that a slowdown in global economic growth rates is already taking place, but despite everything, the IMF is publishing global growth forecasts of 3.5% of GDP. These forecasts have recently been revised downwards, mainly due to the reduction in world trade caused by the tensions produced by the Trump administration. The IMF forecasts for the industrialized economies point to +2.0% and for the emerging economies the forecast is 4.5%. We are facing a scenario of moderation in the growth rate, but we can consider that a global growth of +3.5% is far from a recession scenario.

FACTORS FAVOURABLE FOR FINANCIAL MARKETS IN 2019

Given a perspective of stable economic growth, although with somewhat of a slowdown, we should not enter into recession immediately, much less the scenario in 2008. Obviously, the risks in the financial markets have increased, but it is also true that market valuations are also more attractive after excessive price declines, and where the business profits of the S&P500 companies are expected to grow by 18% and in Europe by 14%. Valuations of the stock and bond markets remain attractive within a scenario of moderate growth. At certain times we will experience periods of volatility, which will offer buying opportunities.

Among the favourable factors, we have sufficient international economic growth rates, with inflation statistics within moderate ranges.

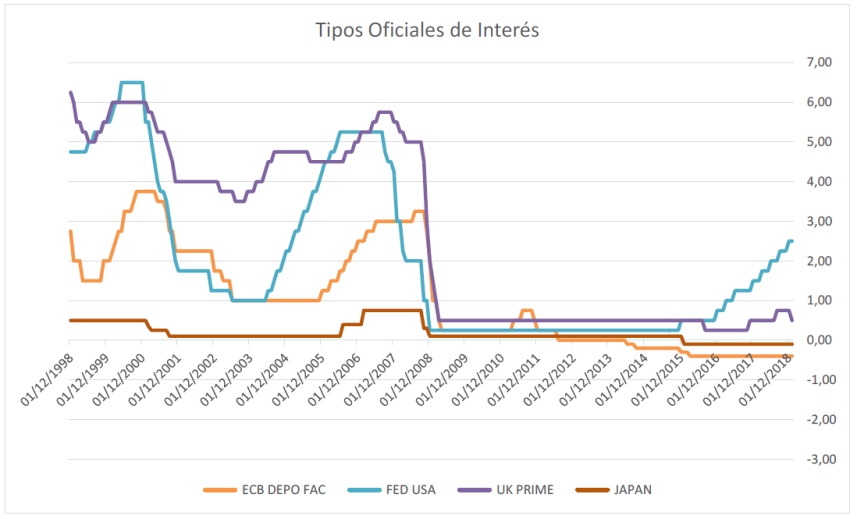

Where the most significant change occurs in 2019 is the position of central banks. The Federal Reserve hinted that, faced with a scenario of moderation in economic growth in the United States, it would be more cautious in the process of rising interest rates. Currently, the interest rate Fed Funds is in 2.50% and the consensus of forecasts indicates that if it does rise, it would not surpass 3%, less than what was discounted previously. The ECB has also announced that it would postpone the possibility of increases until the end of the year and suggested the possibility of applying some special measures. Together, central banks maintain implementing expansive monetary policies.

In conclusion, the Central Banks are going to be a key factor this year, given that sending an aggressive signal to the markets could cause considerable volatility, as in December last year.

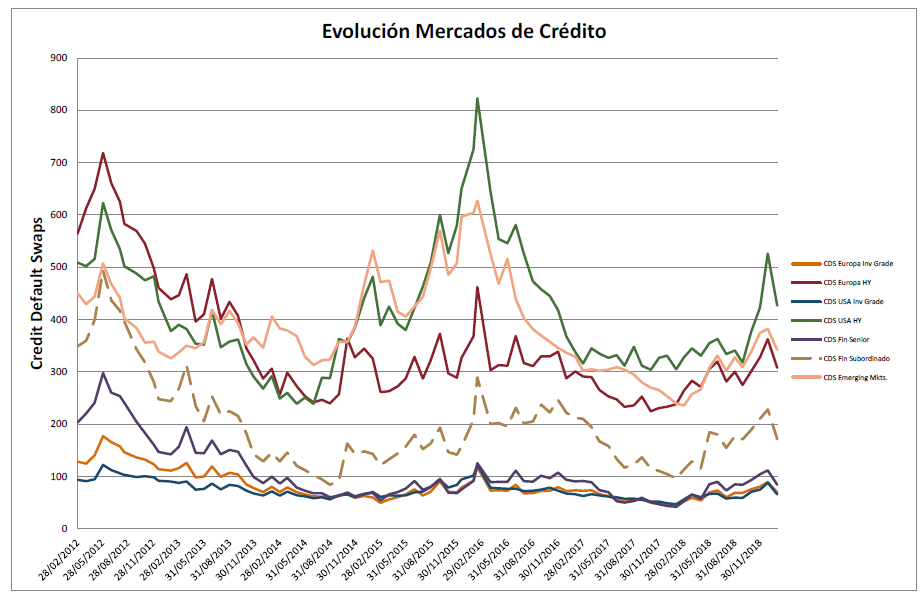

In the fixed income market, the widening of spreads and price drops during 2018 facilitated the appearance of opportunities in the emerging, fixed income, High Yield, fixed income, subordinated financial bonds and the CoCos. In any case, fixed income with a clear preference for short durations, given that there may be a risk of spreads widening. Fixed income issued by governments and fixed income issued by Investment Grade companies is unattractive given that the vast majority of returns in Europe are less than 1%.

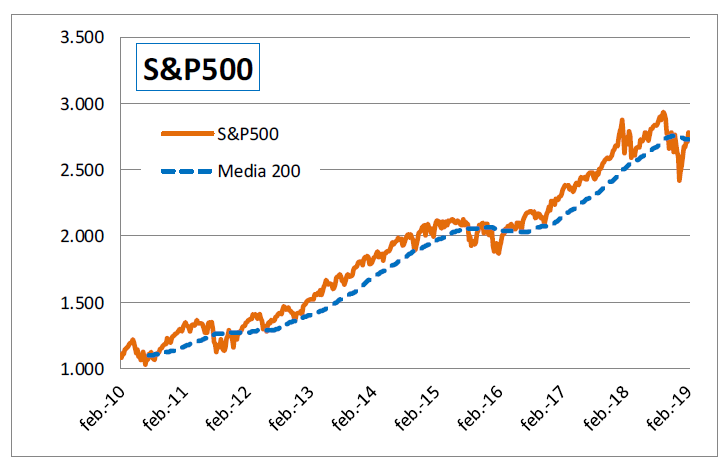

The US equity markets are quoting with more adjusted multiples after the correction of the last quarter of 2018. Estimates of profit growth are over 10% for the next few years and the Federal Reserve has shown signs of moderation in the pace of rises in interest rates, which is favourable for stock markets.

The economy continues to present growth with a moderate slowdown. In this final phase of the cycle, we expect more volatility. Based on the scenarios and multiples, we could consider a range between 2850 and 3100, if a scenario like the one proposed up to now comes to pass. In the case of a higher than expected deterioration, we could place the lower price range at 2400.

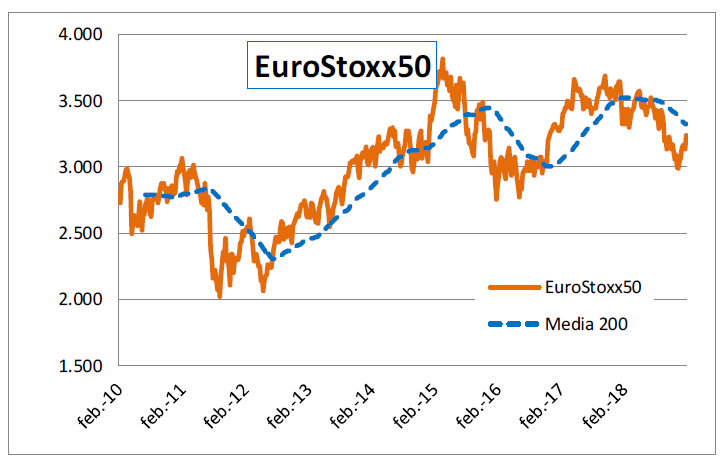

European equity markets are trading at lower multiples, but the estimate of profit growth of listed companies is single-digit.

In Europe, there is a smaller number of companies experiencing growth, with a greater presence of banks and political uncertainties on several fronts (Brexit, Italy, Spain, lower economic growth in Germany and other European countries,...). Based on the estimates we can consider that the EuroStoxx50 could quote at 3,530. In the case of a higher than expected deterioration, we could be at the 3,000 level.

CONCLUSION

Several risks remain alive. In the first place, a breakdown of the negotiations of the trade agreement with China would be bad news and in Europe a hard Brexit would be too. In the US, Trump has only one year to be re-elected, and if he wants to be re-elected he cannot afford a recession. So, time is starting to run against him, and logically he should take actions that reassure the markets.

In conclusion, we have entered the final phase of the economic cycle with a scenario of moderate economic growth. An increase in volatility is more likely, although equity markets are not expensive in their valuations. There is no bubble in stock prices. However, there are too many fronts open that will keep risk premiums high. In any case, scenarios in the 2019 financial markets are more complicated and offer the possibility of building portfolios at attractive prices, taking advantage of corrections.