The economic outlook of the International Monetary Fund (IMF) in January 2016 reduced growth forecasts to 2.1% for the developed countries' economies this year (1.7% for the Eurozone and 2.7% for Spain). Recent Eurostat estimates for the fourth quarter of 2015 confirmed the mediocre expansion in this economic area in 2015, 1.5% (2.4% in the United States).

In the first two months of 2016, market volatility intensified, with sharp declines and fluctuations in stock prices and a resurgence of distrust in the banks' situation in Europe.

The most influential factors in the new situation are, among others, the forced landing of China's economy, the depletion of US growth, which grew only 0.2% in the last quarter of 2015, the presence of signs of weakness in global demand, visible mainly in the sharp falls in the price of crude oil and other raw materials (Nouriel Roubini, 'The global economy new abnormal').

CRUDE OIL

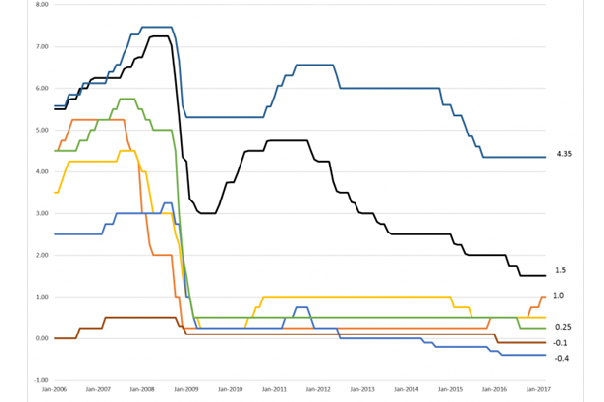

According to this same author, the current situation is characterized by the presence of numerous elements that until quite recently would have been regarded as abnormal, among which the unconventional character of the monetary policy stands out above all. The "quantitative easing" (QE) actions (massive contributions of liquidity to the markets by central banks, which translate into an abundant cash flow in the hands of commercial banks) have become continuous and interest rates have reached negative levels in some cases

In the midst of the banking turmoil that provoked this situation, both the European Central Bank (ECB) and the Bank of Japan have announced new actions, which would intensify the pace of implementation of this policy.

MEDIOCRE EVOLTION OF THE REAL ECONOMY

Stock exchanges have come to register really bullish bubbles in the prices of some assets. This has happened without regard to the mediocre evolution of the real economy. Such a contradictory development would reveal that, in developed and emerging countries, the economy is suffering from an unhealthy situation, which cannot last too long.

Stock markets often anticipate a greater number of recessions than happens in reality, but such signals have become constant and persistent, and more attention has to therefore be paid to what lies behind such warnings. China has built infrastructures with a rate of consumption of cement and concrete that in only two years is equivalent to that of the United States in all of the 20th century. On top of this is the fall in value of its currency, which would have fallen even more if it had not emptied its stock of reserves. China will stop driving the world economy and its debt has multiplied (L. Summers, 'Heed the way of the financial markets', FT, 10.2.2016).

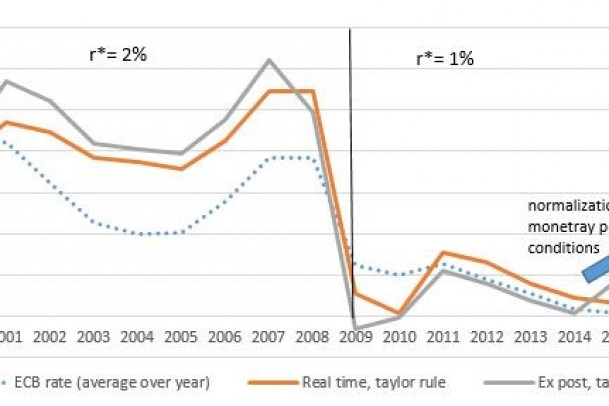

If the Chinese economy declines, the economic policy makers of the United States and Europe will have few instruments to boost global growth. Market expectations for future inflation rule out that the ECB's target for the Eurozone will be accomplished (an inflation rate of 2%). These markets fear negative interest rates and their consequences.

Negative rates reduce the banking business and call into question the situation of many European banks. There appear to be numerous banks that are going to have trouble recovering the significant credits granted to energy-producing companies. Lower profits frighten investors into banking stocks and disrupt the situation of modest savers, who hesitate about where to put their savings.

If the weakness of the Banking Union built in recent years is confirmed, then a single deposit guarantee fund and a greater availability of resources are needed to solve potential banking crises (W. Munchau, "The toxic twins of European finance return', FT, 14.2.2016).

ENCOURAGING FURTHER GROWTH

A variant of the policy followed would be that liquidity provided through quantitative easing could be used to directly finance public expenditure, investment in infrastructures, above all leaving control of the amount issued to central banks. The overall risk to the economy in the United States, Europe and emerging countries is about the same as it was in other previous situations. Those responsible for economic policy should stop hoping for the best and start preparing for the worst (L. Summers, op. cit.).

A recent OECD report also underlines the weak demand, partly explained by the high indebtedness of governments, companies and households. It highlights the growing limitations faced by an economic policy limited almost exclusively to a monetary policy with abundant negative side effects, rather than based on growth.

The adverse context described for the world economy will not help the growth of the Spanish economy. New economic policy has to stop mostly promoting adjustment in salaries and wage devaluation. Fiscal rigour should be compatible with new economic policy actions that favour greater growth.